Get ahead: Why early ISA contributions can make a difference

Discover the benefits of making your ISA contributions at the start of the tax year and how it could enhance your investment growth

The value of investments can fall as well as rise and that you may not get back the amount you originally invested.

Nothing in these briefings is intended to constitute advice or a recommendation and you should not take any investment decision based on their content.

Any opinions expressed may change or have already changed.

Published on 07 Apr 20252 minute read

Investing early in the tax year can significantly boost your individual saving account’s (ISA's) growth potential. By starting your contributions at the beginning of the 2025/26 tax year and beyond, you could allow more time for your savings to benefit from compounding, which can lead to greater long-term wealth accumulation.

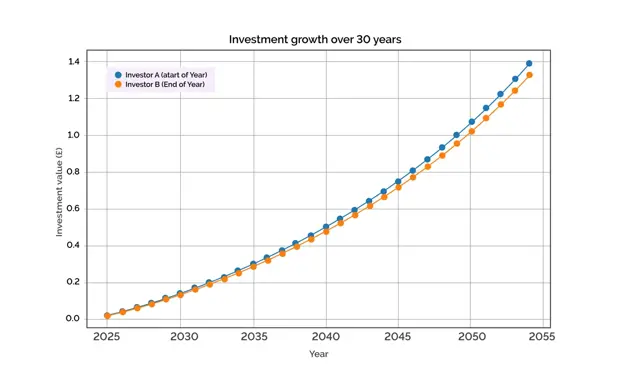

Start at the beginning of the tax year

Research conducted by Bestinvest's parent company Evelyn Partners this month indicates that investing an annual ISA allowance of £20,000 at the start of each tax year (6 April) can lead to a larger investment pot compared to waiting until the end of the tax year (5 April). Many investors still choose to invest at the end of the tax year and in subsequent months, thereby missing out on potential gains. This does, of course, depend on the investments selected and market timing. While investments can go up in value they can also go down and you may not get back the amount invested.

However, an investor who consistently invests at the beginning of each tax year could see their portfolio grow more substantially over 30 years than one who delays their contributions. For example, as illustrated in the chart below, if Investor A invests £20,000 at the start of each tax year on 6 April 2025 and beyond for 30 years, they would be able to accumulate a much bigger pot of money than Investor B, who may instead put their money in at the end of the tax year. If investor A and B both were to get an annual investment return of 5% after fees, their pots after 30 years would accumulate to £1,395,216 and £1,328,777, respectively. It means Investor A will be £66,439 better off in 2055 than Investor B.

This is for illustrative purposes only

Compounding is the key to investment success

If both investors reinvested the returns, they would get an even bigger pot due to compounding. Compounding is best explained with a mathematical example. Let’s say you invest £1,000 in a fund with an annual return of 10%. After the first year, you would have £1,100. In the second year you don’t just earn on the initial £1,000 you invested, but also on the additional £100 gained in the first year, ending up with £1,210.

The principle of compounding means that returns earned on your investments generate additional returns over time, creating a snowball effect. This is why early contributions can be more advantageous, as they provide a longer period for compounding to work its magic. There is no guarantee of returns though as all investing carries risk and investments can still lose value.

Benefits of pound cost averaging

Even if you don't have a lump sum of £20,000 to invest, adopting a method called ‘pound cost averaging’ (PCA) where you make contributions at regular intervals from the start of the tax year can still be beneficial.

PCA or ‘drip feeding’ aligns with the idea that time in the market is more important than timing the market.

There’s no guarantee that, once invested, your money will continue to grow. However, history shows that patient investors that brave the volatile moments by sticking to their investment plan tend to achieve better long-term outcomes.

Looking to make contributions to an ISA early in the tax year?

Don't have an ISA account yet?