Japanese equities have a spring in their step – here’s why

As Japan’s currency slides, we explore what this means and if there are potential opportunities for investors.

The value of investments can fall as well as rise and that you may not get back the amount you originally invested.

Nothing in these briefings is intended to constitute advice or a recommendation and you should not take any investment decision based on their content.

Any opinions expressed may change or have already changed.

Written by Jason Hollands

Published on 05 Jun 20236 minute read

When the world’s most successful investor starts to take an interest in a region, investors may want to take note. With that in mind, Warren Buffet’s recent visit to Japan should encourage investors to re-examine this long-unloved stock market. Investors have been deterred by Japan’s stagnant economy, an ageing and declining population, and its sclerotic corporate culture, but the country is changing.

Buffet first bought shares in Japanese companies in 2020 in the wake of the Covid-related sell-off, but has been topping up this year, saying valuations are low. His Berkshire Hathaway company typically invests in US companies, but bought shares in five Japanese trading houses – Itochu, Marubeni, Mitsubishi, and Mitsui and Sumitumo – in 2020, describing their low valuations as “ridiculous”.

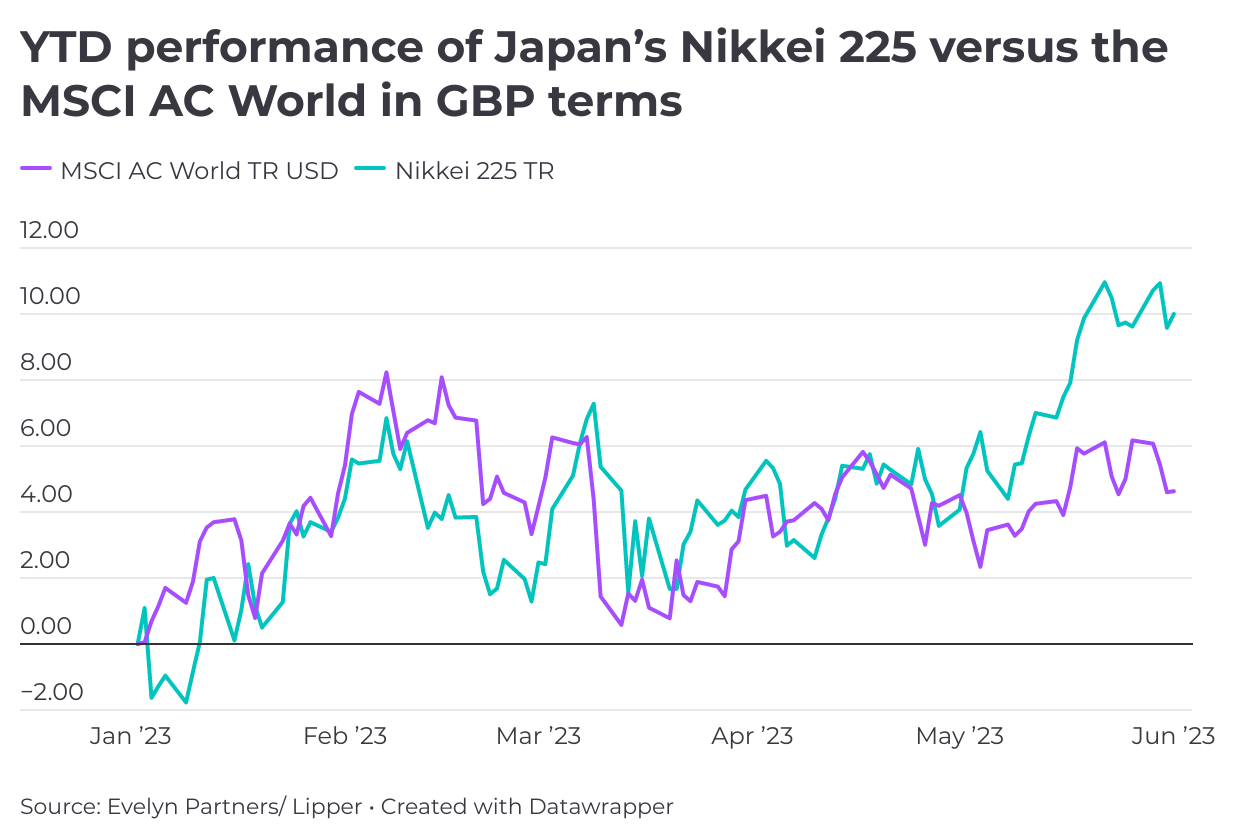

He is not alone in spotting the opportunity. More recently, Japanese equities have been on a tear, with the Nikkei 225 Index surging an impressive 20.6% on a total return basis since the start of the year2 – double that of global equities (the MSCI AC World Index returned 8.9%), taking the Index to a 33-year high.

While things look less dramatic in sterling terms, as underlying share price gains have been offset by a weakening yen and a rebound in the pound. As the graph shows, the sterling return on the Nikkei 225 of 10.0% year-to-date, has still comfortably beaten the sterling returns on the MSCI AC World Index (4.6%) and the S&P 500 Index of US companies (6.4%) and the MSCI United Kingdom Index (2.0%)3.

What explains this new-found interest in Japan?

The weaker yen has undoubtedly been a tailwind. A weak yen has helped improve the global price competitiveness of Japanese exports, which is especially significant for Japan as a major exporter of both vehicles and parts (e.g., Toyota, Honda, Bridgestone), electronics (Sony, Nintendo, Canon, and Kyocera), and heavy machinery (Kubota and Toshiba). A weak yen also boosts the earnings from Japanese companies’ overseas subsidiaries when these are translated back into the yen.

The yen’s weakness has been driven by the Bank of Japan’s continued pursuit of a policy of ultra-low interest rates at a time when many other developed market central banks – including the US Federal Reserve, Bank of England, and European Central Bank – have been aggressively raising interest rates. Interest rates are currently negative in Japan and through its yield curve control policy, the Bank of Japan seeks to cap the yields on 10-year Japanese government bonds at between zero and 0.5%.

For domestic investors, the weak yen and low yields on Japanese bonds are two good reasons to be ploughing savings into domestic equities. A notable development alongside this is a greater propensity for Japanese companies to pay dividends to shareholders. Historically, the Japanese market has been very low yielding as companies were notorious for hoarding cash on their balance sheets. However, this has steadily changed on the back of improving corporate governance standards. Japanese equities – as measured by the Topix Index –are yielding 2.5%4.

Major shake-up of the Tokyo Stock Exchange

Continued weakness in the yen is not guaranteed. The dollar has been softening as markets anticipate an end to the Fed’s rate-hike cycle, and the yen may well strengthen versus the dollar from current levels. However, there are other supports for Japanese equities. Notably, a significant shake-up by the Tokyo Stock Exchange is set to add pressure on Japanese-listed companies to become more shareholder friendly.

A new market structure has been put in place. ‘Prime’ companies are those that meet certain standards of shareholder engagement, while standard companies must have sufficient liquidity and governance levels. Importantly, a new definition of ‘tradeable’ shares excludes holdings by Japanese commercial banks, insurers, and corporations – a move seen to discourage the traditional pattern of cross holdings in the country. Those that don’t comply could face the ultimate sanction of being de-listed.

Importantly, another new requirement is that companies with very low valuations – defined as those where their stock market valuations are lower than the assets set out in their accounts – must set out plans to improve their valuations. This should deter companies from hoarding cash on their balance sheets, encourage higher returns on capital, dividend payouts, share buybacks and lead to greater investment. Over time, this could be a game-changer.

Japanese equities represent the second-largest component of the global equity markets (MSCI AC World Index) when measured by market capitalisation1. It remains an important market. While the easy wins from the yen weakening may be played out, for those who have long ignored Japan, we believe it is a market that deserves some exposure in a diversified, long-term portfolio.

Four popular Japanese equity funds:

- Baillie Gifford Japanese B. This fund, managed by Matthew Brett, looks to invest in stocks that fit in four broad categories: secular growth, growth stalwarts, special situations, and cyclical growth. The top holdings include multinational investment company SoftBank Group, Sumitomo Mitsui Trust Holdings, automation and robotics group Fanuc, and GMO Internet

- Jupiter Japan Income U2. Managers Dan Carter and Mitesh Patel target a relatively concentrated portfolio of circa 40 companies, aiming to achieve a higher yield than the Japanese market. Their approach is flexible enough to blend high-yielding, typically larger stocks, with lower-yielding companies with strong growth potential. Top holdings include Sumitomo Mitsui Financial Group, Sony, as well as Japan’s largest chemical company Shin-Etsu which has the largest global market share in polyvinyl chloride and semiconductor silicon

- JPMorgan Japanese Investment Trust. This trust is managed from Tokyo by experienced managers Nicholas Weindling and Miyako Urabe, supported by a team of over 25 with ‘boots on the ground’ in Japan. Its largest position at 8.1% is electrical appliance group Keyence which makes automation sensors, barcode readers and laser markets, Sony, and insurer Tokio Marine. The trust’s shares currently trade on a -7.7% discount to their net asset value

- iShares Japan Equity Index (UK) D. For investors wanting to take a passive approach that mimics the overall movement of the Japanese market at a low cost, rather than hand the task of trying to beat it by choosing a fund manager, we like this fund which tracks the FTSE Japan Index comprised of more than 500 constituents. This fund has low ongoing costs of 0.08%pa

Need some advice from a Coach?

We’ll be happy to talk you through the investment landscape, analyse your attitude to risk and see what products or investments may be suitable for you. We can also examine whether you’re investing as tax-efficiently as possible.

Sources

1 MSCI AC World Index

2 Lipper, total return in local currency including dividends reinvested, 31/12/22 – 1/6/23

3 Lipper, total return in GBP terms including dividends reinvested, 31/12/22 – 1/6/23

4 JP Morgan Research at 28 May 2023

Important information

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. Details correct at time of writing.

The value of an investment may go down as well as up and you may get back less than you originally invested.

This article is based on our opinions which may change.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data above. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products.

This article is not approved, endorsed or reviewed by MSCI.