Pension or ISA: which is better?

Understand the differences, benefits and drawbacks of investing into a Stocks & Shares ISA vs a pension with this handy overview.

The value of investments can fall as well as rise and that you may not get back the amount you originally invested.

Nothing in these briefings is intended to constitute advice or a recommendation and you should not take any investment decision based on their content.

Any opinions expressed may change or have already changed.

Written by Frances Bruce

Published on 30 Jan 20237 minute read

It’s a classic savers’ conundrum. Pension or ISA: which is better? To use a pension and Stocks & Shares ISA effectively it’s important to understand how they work in different circumstances. We explain everything you need to know here.

ISA vs pension: what’s the difference?

A pension is designed for retirement savings while money held in an ISA can be used for anything. You get generous tax relief when you pay into a pension but pay tax when you take money out of it (apart from the 25% lump sum). An ISA usually gives you immediate access to your money, while money invested in a pension is normally only available when you turn 55 (rising to 57 in 2028).

A standout feature of pensions and ISAs is the tax-free growth you get for your money. You do not pay any tax including dividend tax or capital gains tax on investments held in a pension or ISA.

As always, it’s good to remember that ISAs and pension tax relief and allowances depend on your circumstances and can change without notice. And the value of your investment may go down as well as up, and you may get back less than originally invested.

A comparison: saving into a pension vs Stocks & Shares ISA

Here’s an easy reference table that compares saving into a Stocks & Shares ISA vs a pension plan:

|

|

Stocks & Shares ISA |

Pension |

|

Instant access? |

Yes – but it might take a few days for the funds to be sold |

No access before 55 (unless due to severe ill health or protected retirement age) |

|

Annual contribution limit |

£20,000 |

Every year you can contribute as much into your pension as you have earned, usually up to a maximum of £60,000. If you go over your allowance there will be a tax charge |

|

Tax environment |

Tax-free growth |

Tax-free growth |

|

Tax relief |

None |

20% immediate relief available. Higher and additional tax reclaimable Higher/additional rate taxpayers get further relief via self-assessment |

|

Death benefits |

Full value included in estate for inheritance tax purposes Your husband, wife or civil partner might be able to claim an extra ISA allowance after you die – it’s called the ‘additional permitted subscription’ |

Pension funds not included in value of estate of inheritance tax purposes Tax free on death benefits if paid before deceased’s 75th birthday. Benefits will be subject to beneficiary’s marginal rate of tax if deceased was over 75 at date of death |

Our table above compares investing into a pension vs a Stocks & Shares ISA. There are other factors to consider that depend on your personal circumstances, such as the details of your investment options. An easy way to make sure you’ve considered everything is to get an expert’s perspective before you decide.

Pension or ISA: which is better for retirement?

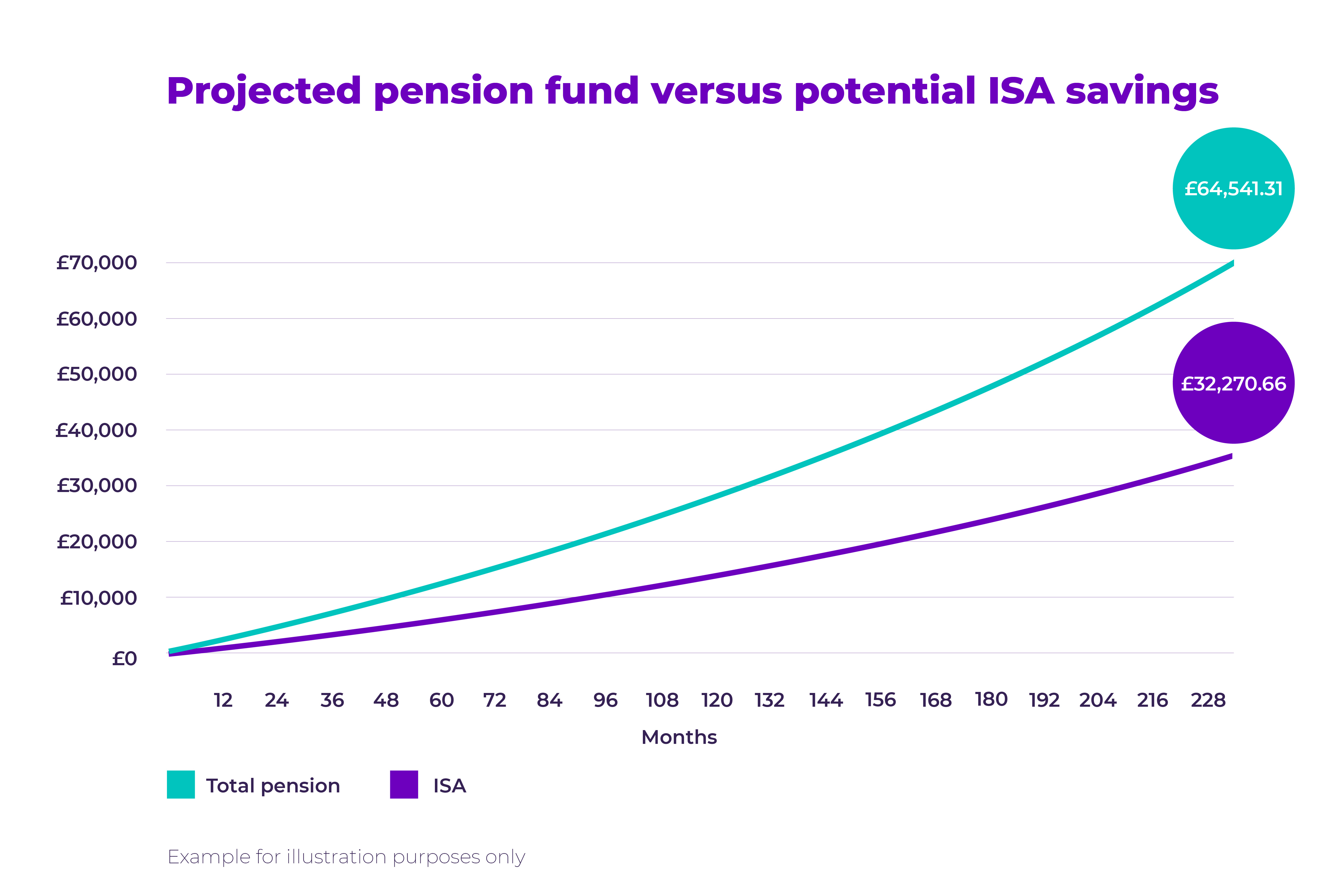

If you have time on your side to save for retirement, you can end up with more savings from your pension than your ISA thanks to the combined powers of tax relief and compounding. Employer contributions can boost your pension savings even more.

Here’s an example of how it can work.

Meet Larry. He earns £30,000 a year and is enrolled in his workplace pension scheme, which requires Larry to pay in a minimum of 5% towards his pension every year. His employer contributes at least 3%.

Larry saves £1,188 (gross) to his pension and his employer adds £712.80. Larry also receives basic-rate tax relief on his pension contributions, so the government tops up his pension savings with £237.60.

That’s right. Larry’s pension pot accumulates £1,900.80 each year but it only costs Larry £950.40. Not a bad return. And some pension schemes offer more.

On the other hand, if Larry saves £950.40 into his ISA – that’s it. No tax relief to bump up his money. No extra 3% employer contributions. That’s why cash and stocks & shares ISAs can’t compete with a pension over the long term.

This chart shows the difference between saving into a pension vs an ISA for retirement:

But what happens if you’re closer to retirement or want to retire earlier than Larry? Let’s look at what you can do to make the most of your money.

Pension or ISA at 50: which is better

When you’re approaching retirement age saving into both a SIPP (self-invested personal pension) or another pension and an ISA can be really helpful. Pension savings are locked away until you’re 55 (rising to 57 in 2028). Stocks & Shares ISAs usually let you access your money straightaway but not all cash ISAs do (allow a few days to sell funds held in a Stocks & Shares ISA).

Do I have to pay tax when I take money out of my pension or ISA?

When you turn 55 (rising to 57 in 2028), you can usually take up to 25% from your pension pot as a tax-free lump sum. You’ll pay income tax at your highest marginal rate for any other withdrawals from your SIPP or pension after that. You don’t pay tax when you take money from an ISA.

Should I use my ISA or pension first?

Savvy investors often use their general investment and taxable accounts first, then their ISA, then their pension. It’s a good idea to protect the tax benefits you get for your pension contributions, and the tax-free benefits of an ISA.

Saving money doesn’t have to be a pension vs ISA situation. Many people invest in both. In fact, one of the common bonds linking successful investors is their willingness to make the most of their tax allowances and invest in a tax-efficient way. We believe an ISA and a pension are excellent options for this.

How Bestinvest can help with your pension and ISA

Our award-winning Stocks & Shares ISA and excellent value Best SIPP can help you achieve your financial goals. With tiered service fees to keep costs down and online share dealing for only £4.95 a trade, it’s easy to set yourself up and maintain your savings.

It’s easy to transfer to us as well. All you need to do is start here. You’ll benefit from our huge range of quality investments and free in-depth guides such as Our top ISA investment ideas and Spot the Dog. We also pay £500 towards exit fees you may be charged when you transfer (T&Cs apply).

And if you're thinking about what’s best for you and your money, why don’t you book yourself in for a free 45-minute coaching session.

At Bestinvest we’re here to make investing affordable and accessible so you can find the fastest path to your financial goals. Let’s go!

Important information

The value of an investment, and the income from it, may go down as well as up and you may get back less than you originally invested.

ISA tax rules can change, and their benefits depend on your circumstances.

Examples of how tax or tax relief may apply are based on our understanding of current tax legislation. Whether any tax will be payable, at what level it is charged and whether you qualify for tax relief will depend upon individual circumstances and may be subject to change in the future.

SIPPs are not suitable for everyone. If you don’t want to invest across different asset classes or don’t think you will make use of the investment choices that SIPPs give you, then a SIPP might not be right for you.

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication.

Pension Transfer Considerations

Before you consider transferring a pension, it is important to ask yourself: Will I lose any valuable benefits or features from my existing pension plan? If the pension is an employer-related plan, will the employer cease to pay in benefits if it is transferred elsewhere? Will I incur any penalties on my existing pension if I transfer? Is it an occupational final salary pension scheme? (in which case it is very unlikely to be advisable to transfer) Have I considered the charges on my current plan? (a new arrangement may be more expensive – especially if you have a stakeholder pension).