Are there opportunities for investors in China and emerging Asia?

Investor optimism for China and emerging Asia is lacking as stock markets lag their developed counterparts and negative news over uncertainty in China continues. But could this mean missing opportunities? This in-depth article from Daniel Casali, Chief Investment Strategist at Evelyn Partners, looks at the significant potential if regional risks subside.

The value of investments can fall as well as rise and that you may not get back the amount you originally invested.

Nothing in these briefings is intended to constitute advice or a recommendation and you should not take any investment decision based on their content.

Any opinions expressed may change or have already changed.

Written by Daniel Casali, Chief Investment Strategist

Published on 07 Jul 20228 minute read

Make Asia great again

On 21 February 1971, US President Richard Nixon made an unprecedented diplomatic mission to China. After stepping off the presidential plane, named The Spirit of ‘76 to capture the self-determination of the American revolution, President Nixon aimed to engage with China economically following years of silence. During meetings the two sides agreed the Shanghai Communiqué, pledging to normalise relations between both countries. It marked the beginning of China’s entrance onto the global stage.

Fifty years on, it seems investors do not view China and emerging Asia with that same optimistic spirit. Emerging Asian stock markets continue to lag developed markets this year following a disappointing show in 2021. China is the main source of this underperformance as it accounts for a hefty chunk of the Asian stock market. The country also dominates trade in the Asia Pacific region, accounting for almost half of Australia’s exports, 28% of Taiwan’s and a quarter of South Korea’s.1

So far this year, MSCI China is down 4% in sterling total return terms, dragged lower by the Government’s zero Covid policy leading to city wide lockdowns.2 Uncertainty generated by the delisting of some Chinese companies from US exchanges led to heavy selling of Chinese stocks by US-based investors. The potential threat of US sanctions should China step in to help Russia and violate current Western sanctions has also weighed on the region. There are also lingering concerns over a potential collapse in China’s property market, whether Beijing invades Taiwan and regulation of the tech sector.

Arguably, much of this negative news is reflected in valuations. The MSCI China is trading on an historically low PE ratio of 11.2 times, while emerging Asian equities are trading below average at a 24% discount to developed markets.3 There is significant potential for emerging Asian equities to outperform developed markets should regional risks subside. Remember that all investments carry risk and investors may get back less than invested.

Monetary policy in China

A key catalyst to revive investor appetite in China is looser monetary policy. It appears that Beijing is pivoting away from the exceptionally tight policy in 2021 and cutting interest rates with the aim of stimulating the economy in 2022. In a marked contrast to a year ago when both regulation and credit were tightened, recent Politburo meetings focused on supporting growth.

This message has already filtered down to other government entities. Chinese regulators have stepped-up stimulus for the important property sector by expanding banks’ mortgage availability and cutting interest rates for the first time in two years.

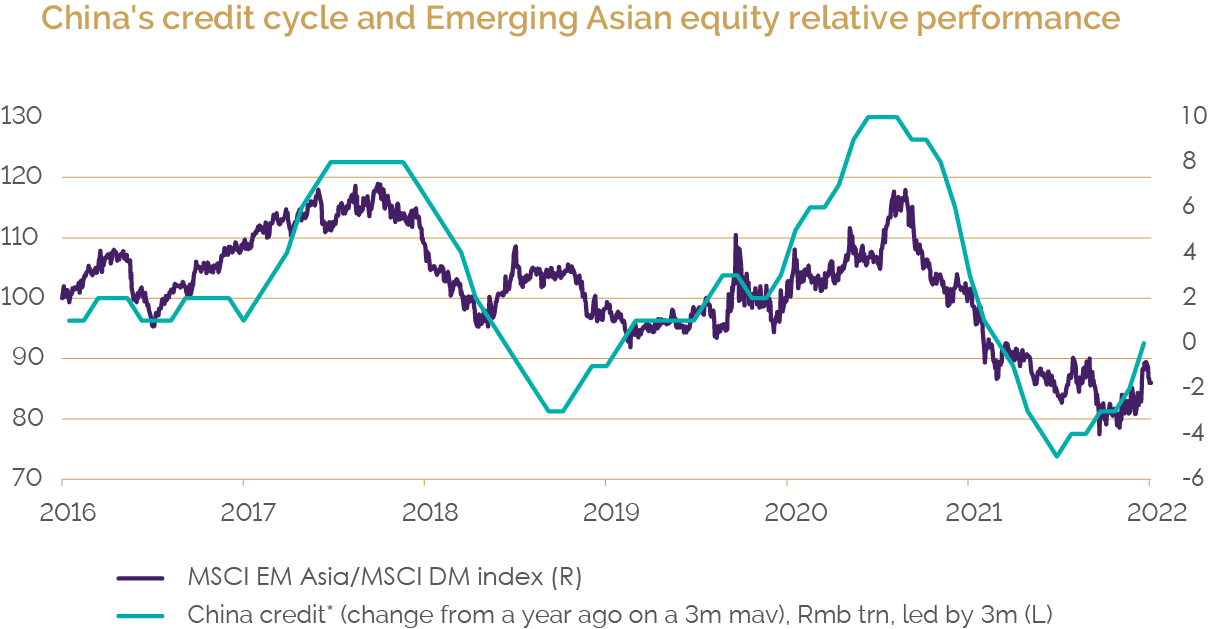

Easing policy in the second-largest economy should also offset the US’s shift to raising interest rates and help sustain the global business cycle. This is already visible in China’s Total Social Finance, compared to a year ago, the data to May shows a clear upswing. The most important thing to note is China’s credit cycle tends to lead to positive performance in emerging Asian equities relative to developed markets.

Source: Refintiv Datastream/ Evelyn Partners, data as at 23 June 2022. Past performance is not a guide to future performance

Critically for ongoing policy easing, inflation in China appears muted:

- Producer price inflation has peaked and there seems little ability for businesses to pass higher production costs onto consumers

- Unlike the US, where the cost of living is increasingly elevated, in China annual CPI inflation is only 2.1%.4 The gap between China and US inflation can be largely attributed to the nature of China’s pandemic policy. Stimulus targeted the corporate sector to boost supply through investment, rather than through raising consumer demand as happened in the US

- China is experiencing less inflation from supply chain bottlenecks than the US. The backlog of orders according to the manufacturing purchasing managers survey is more than 20% higher in the US than China.5 In short, Beijing policymakers have more room to ease policy without the risk of driving up inflation

Looking through the Chinese Covid lockdowns

At the most recent National People’s Congress, the Government set a target for the economy to grow by ‘around 5.5%’ in 2022 in real terms.6 Considering the Covid outbreak this year it may struggle to achieve this. However, given the political importance of the growth target, Beijing is likely to cut interest rates further. Moreover, China’s GDP could well grow by less than the US in 2022, which would be the first time that has happened since 1976 when Chairman Mao died. This is not the economic backdrop China’s leadership will want ahead of its 20th National Party Congress in October, when President Xi is expected to be given an unprecedented third term.

Nevertheless, analysts appear to be balancing the near-term Covid lockdown headwinds on growth with future policy easing in their forecast earnings for Chinese stocks. The Earnings Per Share growth rate for the China Securities Index (CSI) is forecast at 17% for 2022, a steady improvement on the 12% predicted in the summer of 2021.7

Although the recovery in company earnings is not yet reflected in the stock market, there are signs that the sell-off in China could be past the worst. Domestic Chinese-listed value stocks have steadily outperformed growth stocks since the middle of 2021. This is significant as it reflects growing investor optimism that resource and commodity stocks (that sit within the ‘value’ segment) are likely to benefit from policy stimulus driving up economic activity.

The domestic bond market is also signalling stronger growth ahead. The Chinese bond yield curve, which looks at the difference between a bond of 10 years maturity and one of two years, has steepened since towards the end of 2020. Typically, a steeper yield curve is indicative of higher future growth.

Two tail risks

Investing in China comes with plenty of risk. Arguably, the biggest tail risk centres around geopolitics and Covid.

Geopolitics

Fifty years on from President Nixon’s ice-breaking trip to China, today’s fragile Sino-US relations are a risk for Chinese stocks. Russia’s invasion of the Ukraine complicates the relationship between Beijing and Washington. During a discussion with President Xi on 18 March, President Biden formally threatened China that it risked punitive measures if it bypassed sanctions on Russia or supplied military equipment. This looks increasingly likely given China’s growing need for Russia’s natural resources to further its economic development. Energy security is also a huge issue for China: its economy is particularly vulnerable to any restrictions on oil imports via the Persian Gulf by US naval forces. Russia offers an alternative overland route that provides China with some energy security. It appears China and Russia are set to become economically closer over the long term.

Nevertheless, it is encouraging that the US and China continue to talk. China has made it clear it does not want to be drawn into the dispute. China has always upheld the core values of territorial integrity and is publicly concerned at the high number of civilian casualties in the Ukraine. Although Beijing understands Russia’s national border security concerns and its objection to NATO expansion, it may see an opportunity to improve ties with the US and its allies by pushing President Putin to the negotiating table. In pursuit of a diplomatic solution, it is not unthinkable that China might act in a peacekeeping role.

It may also be wrong to draw any parallels between the Russian invasion of Ukraine and any possible military action by China over Taiwan. It is unlikely that China would seek to launch any military adventure while its economy is still so reliant on US semiconductors. In addition, Russia’s experience in Ukraine may make China less inclined to take aggressive action.

Covid policy

Uncertainty continues to present a risk for China’s consumption recovery. This year has seen an uptick in local cases across the country and lockdowns in major cities, such as Shanghai and Shenzhen, have proved economically damaging, hurting retail sales and industrial production.

Even so, there is growing room for flexibility. The Government is aiming to implement a dynamic ‘zero-Covid’ policy, which incorporates mass testing and quick lockdowns to reduce the disruption to the economy. This is a subtle shift from an absolute ‘zero-Covid’ policy. The situation is evolving, but it essentially means that China is moving from a rhetorical ‘zero Covid’ to a de facto ‘living with Covid’.

Premier Li has hinted there could be greater flexibility in dealing with Covid, stating that policies will be “more scientific and precise”.8 This may be a recognition that lockdowns are less effective for the more transmissible Omicron variant. Continued progress in the development, procurement and rollout of vaccines and treatments should open the door to a relaxation and a shift towards ‘living with’ the virus.

In summary

Betting against the second-largest economy could mean missing opportunities. Certainly, there are risks – an over-zealous response to Covid, geopolitical problems and weakening growth – but balanced against fewer inflationary pressures and the proven ability of Chinese policymakers to generate innovation and growth. The short-term turmoil may continue, but the long-term growth trajectory of the region remains intact.

Sources

1,2,3,4,5,7 Refinitiv, Evelyn Partners

6 China sets annual economic growth target at 'around 5.5%', Asia.nikkei.com, 5 March 2022

8 China to adapt to changing Covid situation, China Daily, 11 march 2022

Important information

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. Details correct at time of writing.

The value of an investment may go down as well as up and you may get back less than you originally invested.

Past performance is not a guide to future performance.

Underlying investments in emerging markets are generally less well regulated than the UK. There is an increased chance of political and economic instability with less reliable custody, dealing and settlement arrangements. The market(s) can be less liquid. If a fund investing in markets is affected by currency exchange rates, the investment could both increase and decrease. These investments therefore carry more risk.

Get insights and events via email

Receive the latest updates straight to your inbox.

You may also like…

Market news

2024 Autumn Budget Overview: The key announcements from Chancellor Rachel Reeves

Market news