Are we in an AI bubble?

Since the launch of ChatGPT in November 2022, Artificial Intelligence (AI) has become the defining theme in global equity markets, fuelling a remarkable bull run in US stock market indices. Jason Hollands shares his view on whether we are on the cusp of an AI bubble and if so, what should investors consider?

The value of investments can fall as well as rise and that you may not get back the amount you originally invested.

Nothing in these briefings is intended to constitute advice or a recommendation and you should not take any investment decision based on their content.

Any opinions expressed may change or have already changed.

Written by Jason Hollands

Published on 21 Oct 20258 minute read

Introduction

Since the launch of ChatGPT in November 2022, Artificial Intelligence (AI) has become the defining theme in global equity markets, fuelling a remarkable bull run in US stock market indices.

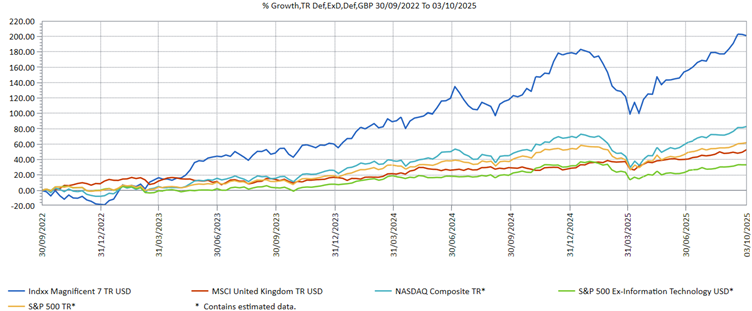

As the chart below shows, over the three years to 3/10/25, the S&P 500 delivered a total return of 62.3 per cent in GBP terms. Yet strip out the technology sector, and that return is halved to 32.8 per cent — well below the 52.8 per cent return from the MSCI United Kingdom index, which has been out of favour with UK investors in recent years.

Past performance is not a guide to future performance.

Source: Refinitiv Lipper

The tech heavy NASDAQ Composite has surged 82.7 per cent, but the real standout has been the Magnificent 7 stocks - Apple, Amazon, Alphabet, NVIDIA, Meta Platforms, Microsoft, and Tesla. The Indxx Mag 7 Index, which has equal-weighted exposure to the seven stocks, returned a staggering 200.7 per cent.

This narrow leadership has created an increasingly concentrated market, with the Magnificent 7 now accounting for nearly 35 per cent of the S&P 500. Such dominance raises a critical question: are we in an AI bubble?

Echoes of the Dot Com era?

The AI rally has drawn comparisons with the Dot Com boom of 1995 to 2000, which turned out to be a classic bubble, which burst spectacularly in the spring of 2000 leading to steep losses for investors who had got swept up in the euphoria.

Particular concerns surround AI poster-child NVIDIA, which makes advanced semiconductor chips, whose share price has rocketed from around $12 three years ago to $185 currently. Some are drawing parallels with Dot Com darling Cisco Systems, a key infrastructure player during the internet boom, which saw its valuation peak at $555 billion with a P/E ratio of around 200x before crashing out of orbit. Today, Cisco is worth $272 billion and has never returned to the lofty valuation it reached during the Dot Com bubble (1).

Valuations for AI-linked stocks are undeniably rich. The S&P 500 trades at 23x forward earnings, compared to 12.9x for the UK’s FTSE 100. NVIDIA’s shares trade at 53.8 times last year’s earnings and 29.9 times projected earnings for the coming 12 months. However, despite its market cap rocketing from $3.3 trillion a year ago to $4.6 trillion currently, it’s valuation based on price/earnings multiple has actually slightly declined from 33.9x a year ago, thanks to earnings growth beating expectations. This is a key distinction from the Dot Com era: today’s AI leaders are profitable, cash-rich businesses, not speculative start-ups.

Bubble characteristics — but not a classic bubble

Historically, bubbles have typically been fuelled by an abundance of cheap money, excessive leverage and speculative fervour. But AI has flourished during a global rate-hiking cycle which has already peaked, and investment has been largely equity-funded, not debt-driven. The scale of capital expenditure is extraordinary: some estimates suggest AI-related spending could hit circa $500 billion next year, covering data centres, cooling systems, and power infrastructure. The hundreds of billions of dollars companies are investing in AI are estimated to account for at least 40 per cent of US GDP growth this year (2).

Yet, while valuations are high, they have yet to reach the irrational levels seen during the Dot Com bubble. Earnings growth has been real and strong, and Price-to-earnings (P/E) ratios have slightly moderated. Still, the risk of a sharp re-rating looms if AI fails to deliver on its transformative promise, if investor enthusiasm wanes or the big players underwhelm growth forecasts. Recent wobbles—such as concerns sparked by Chinese start-up DeepSeek and an MIT report suggesting 95 per cent of firms implementing AI aren’t seeing commercial benefits—show how sentiment can shift quickly (3).

Meanwhile cross-investment and deals between OpenAI – the world’s most valuable start-up at the vanguard of AI development – and leading technology firms, sometimes involving complex financing terms, have raised fears of the sort of circular arrangements which saw connected Dot Com firms collapse like a house of cards.

OpenAI has signed $1tn in deals this year for computing power to run its AI models, including NVIDIA and fellow chipmaker AMD, Oracle and CoreWeave. However, some analysts have warned that OpenAI might never be able to honour these financial obligations.

Where are we in the cycle?

The Dot Com bubble ran for five years before bursting spectacularly in the spring of 2000. So many investors might be wondering: are we in the equivalent of 1995, 1997 or 1999 of the AI cycle? It’s impossible to say with certainty but what is clear is that bubbles can inflate for a long time and often experience short-term pullbacks before resuming their upward trajectory.

During the Dot Com frenzy, the NASDAQ Composite index suffered three major corrections (declines >10%) – in May-July 1996, February-April 1997 and October-December 1997 – as well as a bear market that saw the index drop nearly 30 per cent between July and October 1998.

When the Dot Com bubble finally burst, the S&P 500 fell 47 per cent from peak to trough, and it took until late 2007 to recover. The NASDAQ Composite fell 77 per cent to its October 2002 nadir and took 15 years from then to regain its March 2000 peak. That’s a sobering reminder of the risks that overexposure to hot themes can carry.

US technology stocks have seen significant volatility in recent years. The Covid crash of early 2020 and subsequent boom in tech stocks was an exceptional period in equity markets, with the bull market turbocharged by record low interest rates, huge money printing and people working, shopping and entertaining themselves online during the lockdowns. There was then a major correction in 2022, which was by some measures a bear market and aggravated by a concurrent reversal in bond prices. The Mag 7 index had plunged by 45 per cent from its post-Covid peak by the time this correction played out, so that was a moment when it felt like the tech bubble had burst (4).

But then AI came to the rescue with the launch of ChatGPT, and the last significant correction – but brief - was the Trump induced tariff crash in April this year, which also entered bear market territory for some indices. AI might be a paradigm shift in technological innovation and in its impact on businesses, but many investors are wrestling with whether it is also a new phase in the stock market cycle.

Tread carefully

We are not in the camp that believes you can accurately predict imminent crashes — such calls are usually wrong. But we do believe in caution when valuations are stretched.

Many investors are heavily exposed to US equities and the ‘Big Tech’ AI darlings, often through market-cap weighted passive funds like those which track the S&P 500 as well as global trackers. If the AI rally reverses, these investors could face painful losses given the record level of stock concentration. The S&P 500 may include 500 companies, but when NVIDIA alone represents nearly 8% of the index and ten companies represent nearly 39%, the diversification benefits of a tracker are a bit of an illusion.

It could also be wise to rebalance portfolios that have become too heavily weighted towards the US, by diversifying towards other regions like the UK, Europe, Japan, and emerging markets.

That doesn’t mean abandoning the US: it remains home to world-class companies and is too important to ignore. But it’s wise to review the types of funds you hold for US exposure.

If you’re entirely in market-cap weighted trackers, one option could be to switch some of that exposure to equal-weighted funds, such as the Xtrackers S&P 500 Equal Weight UCITS ETF or Legal & General S&P 500 US Equal Weight Index I. This reduces concentration risk as each company in the index gets a 0.25 per cent weighting, which means you will not be heavily exposed to the ‘big tech’ stocks. During the Dot Com crash, equal-weighted strategies proved much more defensive and went on to outperform for years.

Another possible alternative could be to rotate into valuation-conscious active funds, such as the Dodge & Cox US Worldwide Stock Fund which is actively managed, or the Invesco FTSE RAFI US 1000 ETF which own the thousand largest US companies but weights them on four fundamental factors (sales, cash flow, book value and dividends) rather than market-cap.

Finally, as a correction or bear market in US equities usually tiggers some contagion globally, it could be a good time for investors to review their overall equity exposure and consider whether – given their investment timeline and needs – they are sufficiently diversified into other assets like bonds, gold and infrastructure.

Investments carry risks and you may get back less than you invested. Funds that invest in specific sectors may carry more risk than those spread across a number of different sectors. In particular, gold, technology and other focused funds can suffer as the underlying stocks can be more volatile and less liquid.

Final thoughts

AI is a powerful theme, and its long-term impact is likely to be profound. The same was true of the development of the railways in the nineteenth century and the world wide web at the cusp of the millennium - both of which saw speculative investment bubbles that burst leading to huge losses of capital. Excitement about AI has created pockets of froth, concentration risk and current valuations are pricing in huge optimism about growth ahead. Diversification — across geographies, sectors, and strategies — is your best defence.

Get a refresher on diversification and why it matters

Book a free session with one of our Investment Coaches to brush up on diversification and what factor it plays in building your investment portfolio. Our coaches can provide guidance and support but can’t give you specific investment advice.

Sources

(1) Bloomberg

(2) The Economist

(3) Forbes

(4) Refinitiv, Lipper