Down with the dollar

The falling US Dollar Index (DXY) has been generally positive for stock markets. Could this signify the end of the weak dollar? Or just the beginning?

The value of investments can fall as well as rise and that you may not get back the amount you originally invested.

Nothing in these briefings is intended to constitute advice or a recommendation and you should not take any investment decision based on their content.

Any opinions expressed may change or have already changed.

Written by Daniel Casali, Chief Investment Strategist

Published on 21 Jun 20235 minute read

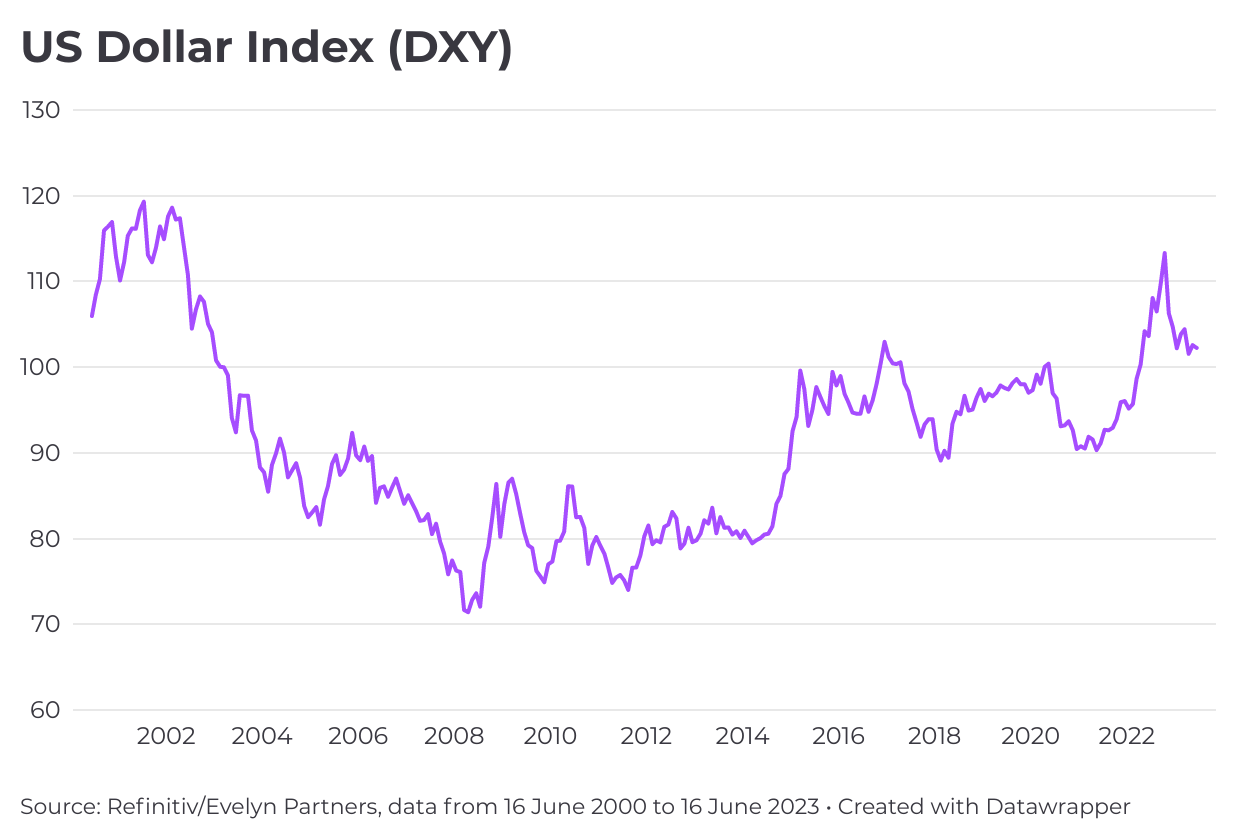

A weakening US dollar has been a feature of financial markets since October 2022. The US Dollar Index (DXY), which looks at the value of the dollar versus a basket of other currencies, has fallen around 10% from its peak.1 This has generally been positive for stock markets, by creating additional market liquidity that has supported share prices. However, is this dollar weakness at an end? Or just beginning?

Short-term factors

There are a number of short-term factors (i.e. over the next 6-12 months) that have created downward pressure on the US dollar. It gained significant ground during the pandemic as investors sought a safe haven, pushing its valuation (relative to other currencies) to a 20-year high. Until last autumn this strength continued, fuelled by widespread risk aversion and fears over recession. This left it looking expensive and due for a reset.

An improvement in the economic outlook has brought about that change. The US dollar is a counter-cyclical currency – strengthens in times of risk aversion and generally weakens at times of improving economic growth. There has been a stronger global recovery than expected, with Europe avoiding an energy crisis, China re-opening and the remarkably resilient US consumer. This has improved investor sentiment and the risk aversion, which characterised 2022, has been reversed, which is bad news for the ‘safe haven’ dollar.

There has also been a narrowing in interest-rate differentials. The Federal Reserve had been aggressive in raising interest rates, but other countries are catching up as the US pauses. The US Central Bank may continue to signal further interest-rate rises, but we believe it is edging closer to the peak.

Reviving world growth

The US dollar has also responded to the adjustment in the balance of world economic growth. While the US led the global economy as it emerged from the pandemic, more recently growth in the rest of the world has started to pick up and challenge, or even outpace, that of the US.

There are still mitigating factors. For example, foreign capital is flowing into US assets, possibly due to the boom in artificial intelligence (AI). However, this may only provide marginal support for the dollar and other factors are likely to prove more important.

Long-term outlook for the dollar

The longer-term picture (i.e. over the next 10 years) for the US dollar is more complex. There are challenges to the dollar’s position as the world’s reserve currency. China is snapping at the US’s heels as the largest and most powerful economy in the world.

The renminbi is increasingly used for trade, a phenomenon that has accelerated since Russia's invasion of Ukraine. China and Russia have started to trade between themselves in their own currencies, following Russia’s expulsion from the global financial system. In March, Brazil and China reached an agreement on a renminbi-based trade deal. The importance of the ‘petrodollar’ is declining with China now by far the largest importer of Saudi oil. Even France has recently bought liquefied natural gas (LNG) in renminbi. With China’s share of global goods trade now around 15%, this is an increasingly powerful force.1

There are some concerns that as emerging economies grow and have an increasing share of global economic activity they could come together and form a new global currency. However, this group of countries is very diverse, it includes Brazil, Russia, China, and India, along with many others, and they do not share similar views and policies.

The US dollar does look unattractive in its valuation compared to other major currencies. On a fair value basis going back over 40 years, sterling looks extremely cheap compared to the US dollar. There is room for sterling to appreciate against the dollar in the long term.

Could the US dollar lose its role as a reserve currency?

Whilst there are clearly near-term and long-term pressures on the US dollar, we do not think this means it will lose its role as a reserve currency.

The US dollar commands a huge share of the financial system: its role in international debt securities and cross-border loans is vast. For the most part, there is no alternative. It also boasts greater capital market liquidity than any other country, the US has a larger debt market and continues to issue government bonds to support its vast trade deficit. The US is also an open trading partner (though China and Russia may disagree) and this gives the dollar a clear advantage.

In contrast, the availability of renminbi outside of China is $120 billion which pales in comparison to the $57 trillion for the eurodollar market (i.e. dollars held outside the regulation of US authorities) at the last count in 2018.2 The country runs strict capital controls which in the past have helped China maintain financial stability but are a severe hindrance in is efforts to internationalise the renminbi.

Even if these limitations were lifted, it is difficult to see a swift adoption of the renminbi by, say, European powers, who are substantially politically aligned with the US. This puts a natural brake on renminbi strength.

Ultimately, the network effect is likely to support the dollar’s role as the world’s reserve currency for a long time to come. Countries want ease of trade and will use the currency that their trading partners are using. For the most part, this is still the dollar.

Our view is that over the next year, the US dollar will continue to depreciate as its recent run of strength and over-valuation unwinds. The dollar retains its reserve currency status but falls in value. So, it may still be a case of down with the dollar.

Sources

1 Refinitiv/ Evelyn Partners, data as at 16 June 2023

2 Shah, R., "Down The Rabbit Hole" - The Eurodollar Market Is The Matrix Behind It All, RS Advisories, 15 April 2020

Important information

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. Details correct at time of writing.

The value of an investment may go down as well as up and you may get back less than you originally invested.

Past performance is not a guide to future performance.