Global markets – was last week the ‘acceptance’ phase?

COVID-19 seems to be subsiding in China but accelerating elsewhere. Cutting and running may not be the correct medium-term strategy – the markets are trying to come to terms with the shock and consolidate

The value of investments can fall as well as rise and that you may not get back the amount you originally invested.

Nothing in these briefings is intended to constitute advice or a recommendation and you should not take any investment decision based on their content.

Any opinions expressed may change or have already changed.

Written by Andrew Ramsbottom

Published on 10 Mar 20203 minute read

After the precipitous falls of late February, this week saw volatile but basically directionless equity markets. Sovereign bond yields have continued to fall and are now at or close to all-time lows.

What is going on?

Equities

The weakness in late February was largely technical, led by futures-related selling and repositioning. This was the fastest correction in stock market history, whereas last week was more real, i.e. long only and retail.

Behavioural theory is the best way to explain what’s happening. The underlying fundamentals are largely irrelevant: human emotions react to change in four distinct stages.

Reacting to change

|

Stage |

1 |

2 |

3 |

4 |

|

State |

Status Quo |

Disruption |

Exploration |

Rebuilding |

|

Reaction |

Shock/ Denial |

Anger/ Fear |

Acceptance/ Exploration |

Embrace new environment |

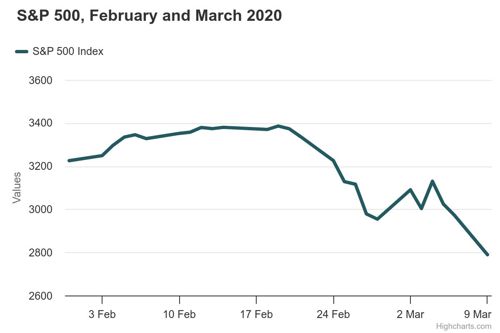

Denial (stage one) was the period up to the last week in February. Panic (stage two) was the last week in February. Last week there was an attempt at acceptance (stage three), however Saudi Arabia’s disagreement with Russia over how to fix the oil price has resulted in it falling sharply, creating further short-term financial market volatility today. This can be seen in the S&P 500 chart below (source: Bloomberg).

Bonds

The Federal Reserve (Fed) cut US interest rates by 0.5% on Tuesday. Sovereign bonds are anticipating further cuts, in particular:

- another 0.5% by the Fed at their meeting on 18 March, then another 0.25% later

- 10bp by the European Central Bank (ECB) at their meeting on Thursday, 12 March

- 0.25% by the Bank of England on 26 March plus possibly another 0.25% later

What are investors looking for?

Investors want signs that the authorities have got things under control, in particular that they can contain the spread of the virus. This is the US$64 million question: Coronavirus seems to be subsiding in China but still accelerating elsewhere; will isolation work, or will it prolong and worsen the impact? Only time will tell. In the meanwhile, the resulting uncertainty is hurting markets.

Another important sign for investors would be the evidence that the authorities can contain the economic impact.

We have seen what is anticipated from monetary policy (ie interest rates). However, equities fell after last week’s Fed rate cut. Monetary policy is running out of road. More practical, direct solutions are needed, and we are beginning to see them.

COVID-19 measures around the world

China has been steadily offering targeted help, especially to small businesses.

In the US, the House announced a US$7.8 trillion Emergency Spending Bill on Wednesday. There are hints of more to come and of widening the Fed’s brief. Also, Trump has an election to win in November.

The Bank of Japan is intervening in the equity and government bond markets, while in the UK we are already spending on infrastructure. More plans will probably be revealed in Wednesday’s Budget.

Europe is notably absent from this list, at the moment.

Helicopter Money has arrived in Hong Kong, Indonesia and most recently Australia.

Should we be doing anything?

There was a special meeting of Tilney’s Asset Allocation Committee on Friday. The main takeaways were that this is obviously not a normal crisis. It has important direct potential implications for the real world.

As per our reaction theory, the markets are trying to come to terms with the shock and consolidate. We now appear to be in the eye of the storm.

A recovery, when it materialises, is likely to be U rather than V shaped. Given the sudden and brutal nature of the sell-off, most long-term investors didn’t 'lighten up' ahead of the correction.

At the moment, it’s probably too early to be aggressively averaging down or taking advantage of the market weakness.

This is not the time to panic. If we thought our clients needed to do anything, we would have contacted them or done it. History shows that cutting and running after a market setback such as this one is not usually the correct medium-term strategy. Keep calm and carry on.

If you have any questions about your investments, or the markets, please do not hesitate to get in touch with your usual Tilney contact or call us on 020 7189 9999.

Get insights and events via email

Receive the latest updates straight to your inbox.

You may also like…

Market news

2024 Autumn Budget Overview: The key announcements from Chancellor Rachel Reeves

Market news