Power to the corporates

Some businesses benefitted from the higher-inflationary environment. Can consumers afford the higher prices for much longer? This article takes a closer look at corporate pricing power.

The value of investments can fall as well as rise and that you may not get back the amount you originally invested.

Nothing in these briefings is intended to constitute advice or a recommendation and you should not take any investment decision based on their content.

Any opinions expressed may change or have already changed.

Written by Daniel Casali, Chief Investment Strategist

Published on 24 May 20234 minute read

The resilience of corporate earnings has been one of the more surprising features of the past 12 months. Despite the biggest interest rate rises in 40 years, geopolitical tensions and the looming threat of recession, earnings have been largely flat. Much of the corporate sector has shown real and sustained pricing power, allowing them to improve profit margins and deliver stronger earnings.

What is pricing or market power?

Pricing power, also known as market power, is when a business can raise the price of an item without it materially impacting demand. This then increases their profits.

Where does pricing power come from?

In many cases, this pricing power has its roots in the pandemic. Lockdowns across the globe brought supply shocks, bottlenecks and shortages of goods. Businesses have taken advantage of a higher-inflationary environment to increase the prices charged for goods and services. This corporate pricing power has enabled firms to offset rising input costs, such as wages and materials.

That said, some sectors may benefit more than others. In general, companies with more monopolistic characteristics have been in a better position to pass on rising prices. That includes sectors such as energy, technology (particularly semiconductors) and materials. Sectors such as real estate, utility and consumer discretionary companies have found it more difficult to raise prices.

The latest performance from corporates

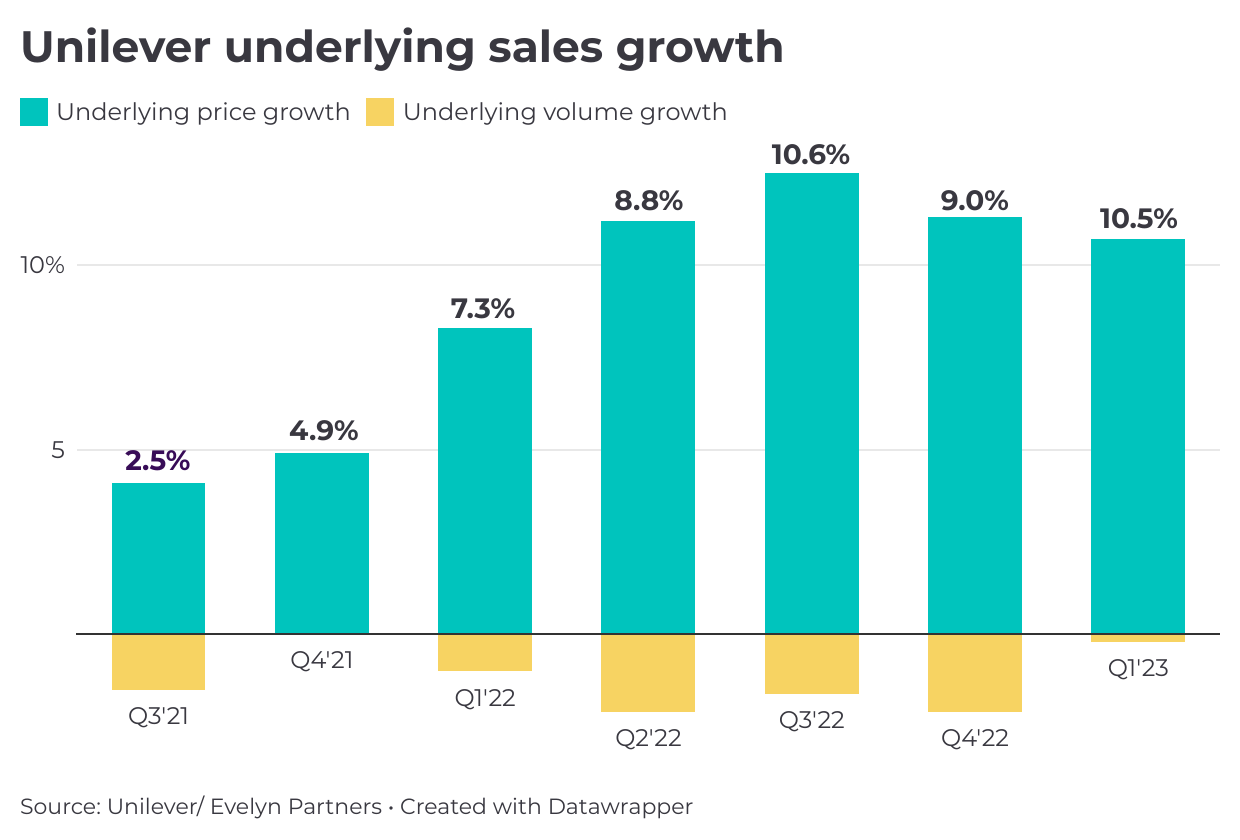

The latest earnings season has shown clear evidence of this pricing power. Unilever, for example, has seen flat volume growth but has been able to raise prices by over 10%. Nestlé has pushed its prices up 10% in the year to March 2023, while Coca-Cola raised its prices 16% in 2022 and plans to raise them a further 13% this year1. A similar phenomenon is happening in the services sector - Aston Villa, for example, increased its ticket prices by 15% for next season2.

This is not just a phenomenon for branded goods. In fact, price rises for staples and own-brand labels have outpaced their branded rivals in many cases. Own-brand baked beans, for example, are up more than Heinz, while Asda butter has shown stronger price rises than Lurpak2. The phenomenon of shrinkflation is also in evidence in everything from crisps, tissues and washing powder.

What is shrinkflation?

Shrinkflation is another way companies demonstrate their pricing power by reducing the package size of their goods but continuing to charge the same price. Smaller packets or fewer items in those packs are less noticeable than raising prices. Even less obvious is companies start to cut corners on their products, such as reducing some ingredients in favour of cheaper alternatives. All have the same effect: passing on the price rises to the consumer.

Will consumers be able to afford higher prices long term?

For the time being, it appears that there is still some slack in the system. An examination of real household purchasing power in the US (which considers various income sources, including labour earnings, dividends, social transfers, consumer credit and wealth from housing) found that it is still growing, albeit below its long-term average (3.3% versus 3.7%)3. Corporates recognise that they can pass on higher costs.

The impact of weaker property prices is also a factor. Property prices have wobbled and, in the past, this has exerted a dampening effect on consumption, particularly in countries such as the UK where a lot of wealth is tied up in housing. If there were a significant slowdown in consumption, it would be increasingly difficult for companies to raise prices.

Sales levels remain resilient, suggesting that higher prices aren’t deterring consumers. This is particularly true when compared to previous shocks, such as the global financial crisis or pandemic. Relatively sticky inflation continues to give corporates the cover to raise pricing power. Equally, product shortages remain and may take a number of years to normalise.

As such, we can see continued strength in corporate profit margins. While some deceleration in growth is likely, profit margins remain a long way from historical averages and look well-supported. Analysts are expecting 10-11% earnings growth for 2024 and 2025, respectively, with corporate pricing power giving a broad-based lift to earnings4. We expect listed companies globally to show resilience and come close to these EPS forecasts.

In reality, the pandemic has worked in favour of corporates. Individuals may now be experiencing a cost-of-living crisis, but it is a cost-of-living boom for the corporate sector. They have managed to pass on rising prices and shore up their profit margins. This should be supportive for stock markets in the year ahead.

Sources

1 BBC News / Reuters

2 Michael, D., Aston Villa: Season ticket rise 'seems excessive and out of step', BBC Sport, 25 April 2023

3 www.trolley.co.uk

4 Refinitiv / Evelyn Partners

Important information

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. Details correct at time of writing.

The value of an investment may go down as well as up and you may get back less than you originally invested.

This article is based on our opinions which may change.