Why small monthly pension contributions can make a big difference

Pensions are long-term investments. You may get back less than you originally paid in because your capital is not guaranteed and charges may apply.

Small contributions add up over time

Most people can’t afford to pay a big lump sum into their pension. Fortunately there is an excellent alternative – making smaller, regular contributions each month. If you are auto-enrolled in a workplace pension you’re already doing this. But if you’re not, or you’d just like to save more for retirement each month, it’s a good idea to set up monthly contributions into a personal pension.

Even if you can’t afford to contribute hundreds of pounds each month, it still makes sense to pay in what you can. This is because even small amounts can add up significantly over time – especially with a long-term investment like a pension.

The effects of compounding

How do these smaller, regular contributions make such a big difference? Through the power of compounding. Albert Einstein reportedly called compounding the 8th wonder of the world – but in layman’s terms it’s the snowballing effect of your returns generating more returns. And the longer your money is invested, the bigger effect it can have on your pension.

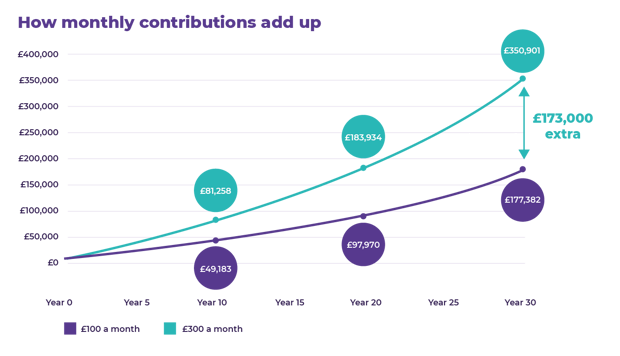

It pays to pay in as much as you can

To get an idea of how quickly monthly contributions can add up over time, take a look at the below chart. It shows two £20,000 pensions growing by 5% a year over 30 years. One has £100 paid into it each month, and the other has £300.

This graph is based on monthly contributions of £100 and £300 plus investment returns of 5% per annum, exclusive of any fees (which may vary from provider to provider), compounded monthly. All figures quoted are for illustrative purposes only.

Of course the £300-a-month pension has grown much bigger than the £100-a-month equivalent. After all, more money is being paid into it each month. But with the power of compounding, it is also growing at a much faster rate (which we can see in the much steeper line).

The message from this is clear – if you can afford to pay more into your pension each month, you should. Even a small monthly increase can make a big difference over several decades.

Making monthly contributions with Bestinvest

With the Best SIPP - our award-winning personal pension – it’s easy to make monthly contributions. The money will come out of your bank account each month, and you can choose to either deposit it as cash or invest into funds. The whole process is automatic – once you’ve set it up, you don’t have to lift a finger. The minimum contribution is £50 a month, which is topped up to £62.50 after 20% tax relief from the Government.

Open a Best SIPP*

You can open a Best SIPP and start making monthly pension contributions easily. Just find your bank details and National Insurance number, and then complete our online application form to open your SIPP. You’ll be asked whether you want to pay in a lump sum or set up monthly savings – you can choose either or both.

If you have several pensions with other providers, you could get more control over your retirement savings by transferring** them all into one SIPP account. And when you transfer them to Bestinvest, we will do all the legwork for you and pay you up to £500 towards any exit fees your other providers charge***.

Further details

The value of an investment may go down as well as up, and you may get back less than you originally invested.

Prevailing tax rates and reliefs depend on your individual circumstances and are subject to change.

This article does not constitute personal advice. If you are in doubt as to the suitability of an investment please contact a financial adviser

*SIPPs are not suitable for everyone. If you don’t want to invest across different asset classes or don’t think you will make use of the investment choices that SIPPs give you then a SIPP might not be right for you. Please contact us for guidance or advice if you are unsure whether a SIPP is right for you.

**Before you consider transferring a pension, it is important to ask yourself:

- Will I lose any valuable benefits or features from my existing pension plan?

- Will I incur any penalties on my existing pension if I transfer?

- Is it an occupational final salary pension scheme? (In which case it is very unlikely to be advisable to transfer).

- Have I considered the charges on my current plan? (A new arrangement may be more expensive – especially if you have a stakeholder pension).

- Have I checked the investment options available and whether I need the wider choice offered by a SIPP?

- If the pension is an employer-related plan, have I checked if the employer will cease to pay in benefits if it is transferred elsewhere?

Recent articles

View all articlesNeed more help?

If you can't find the answer to your question, get in touch or we'll be happy to call you.